Page 68 - Economic report 2020

P. 68

contrasting with the situation in the period 2017-2021, when it represented 68% on average,

compared with 32% short-term debt. In this context, the International Monetary Fund (IMF) has

supported the fiscal discipline process which has enabled Andorra to reduce public debt and meet

the fiscal targets set for 2022.

1.1. Revenue

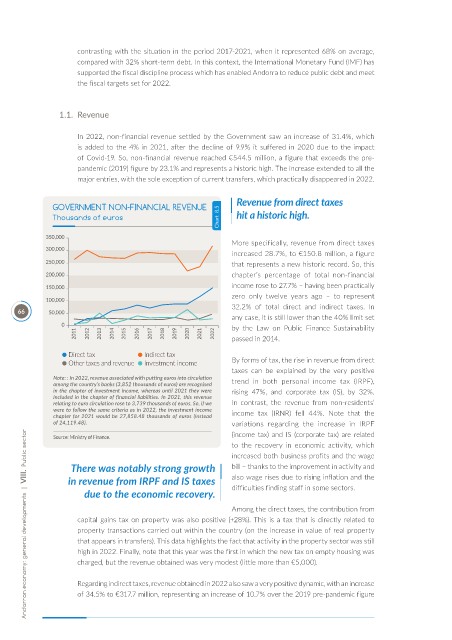

In 2022, non-financial revenue settled by the Government saw an increase of 31.4%, which

is added to the 4% in 2021, after the decline of 9.9% it suffered in 2020 due to the impact

of Covid-19. So, non-financial revenue reached €544.5 million, a figure that exceeds the pre-

pandemic (2019) figure by 23.1% and represents a historic high. The increase extended to all the

major entries, with the sole exception of current transfers, which practically disappeared in 2022.

Revenue from direct taxes

GOVERNMENT NON-FINANCIAL REVENUE

Thousands of euros Chart 8.5 hit a historic high.

More specifically, revenue from direct taxes

increased 28.7%, to €150.8 million, a figure

that represents a new historic record. So, this

chapter’s percentage of total non-financial

income rose to 27.7% – having been practically

zero only twelve years ago – to represent

32.2% of total direct and indirect taxes. In

66

any case, it is still lower than the 40% limit set

by the Law on Public Finance Sustainability

passed in 2014.

Direct tax Indirect tax

Other taxes and revenue Investment income By forms of tax, the rise in revenue from direct

taxes can be explained by the very positive

Note: : In 2022, revenue associated with putting euros into circulation trend in both personal income tax (IRPF),

among the country’s banks (3,852 thousands of euros) are recognised

in the chapter of investment income, whereas until 2021 they were rising 47%, and corporate tax (IS), by 32%.

included in the chapter of financial liabilities. In 2021, this revenue

relating to euro circulation rose to 3,739 thousands of euros. So, if we In contrast, the revenue from non-residents’

were to follow the same criteria as in 2022, the investment income income tax (IRNR) fell 44%. Note that the

chapter for 2021 would be 27,858.48 thousands of euros (instead

of 24,119.48). variations regarding the increase in IRPF

Andorran economy: general developments | VIII. Public sector

Source: Ministry of Finance. (income tax) and IS (corporate tax) are related

to the recovery in economic activity, which

increased both business profits and the wage

There was notably strong growth bill – thanks to the improvement in activity and

in revenue from IRPF and IS taxes also wage rises due to rising inflation and the

due to the economic recovery. difficulties finding staff in some sectors.

Among the direct taxes, the contribution from

capital gains tax on property was also positive (+28%). This is a tax that is directly related to

property transactions carried out within the country (on the increase in value of real property

that appears in transfers). This data highlights the fact that activity in the property sector was still

high in 2022. Finally, note that this year was the first in which the new tax on empty housing was

charged, but the revenue obtained was very modest (little more than €5,000).

Regarding indirect taxes, revenue obtained in 2022 also saw a very positive dynamic, with an increase

of 34.5% to €317.7 million, representing an increase of 10.7% over the 2019 pre-pandemic figure