Page 66 - Economic report 2020

P. 66

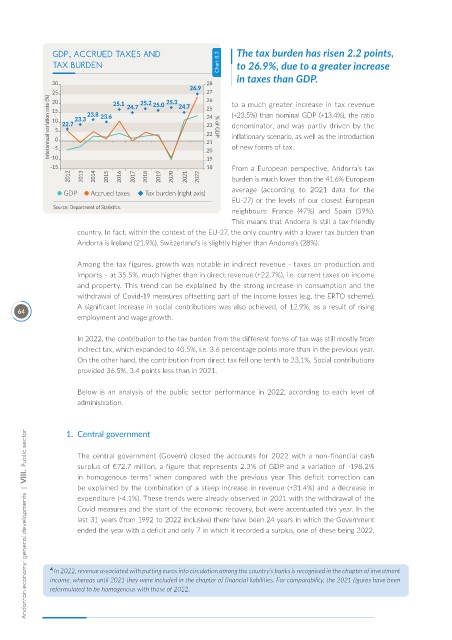

GDP, ACCRUED TAXES AND The tax burden has risen 2.2 points,

TAX BURDEN Chart 8.3 to 26.9%, due to a greater increase

in taxes than GDP.

to a much greater increase in tax revenue

(+23.5%) than nominal GDP (+13.4%), the ratio

denominator, and was partly driven by the

inflationary scenario, as well as the introduction

of new forms of tax.

From a European perspective, Andorra’s tax

burden is much lower than the 41.6% European

GDP Accrued taxes Tax burden (right axis) average (according to 2021 data for the

EU-27) or the levels of our closest European

Source: Department of Statistics.

neighbours: France (47%) and Spain (39%).

This means that Andorra is still a tax-friendly

country. In fact, within the context of the EU-27, the only country with a lower tax burden than

Andorra is Ireland (21.9%). Switzerland’s is slightly higher than Andorra’s (28%).

Among the tax figures, growth was notable in indirect revenue - taxes on production and

imports – at 35.5%, much higher than in direct revenue (+22.7%), i.e. current taxes on income

and property. This trend can be explained by the strong increase in consumption and the

withdrawal of Covid-19 measures offsetting part of the income losses (e.g. the ERTO scheme).

A significant increase in social contributions was also achieved, of 12.9%, as a result of rising

64

employment and wage growth.

In 2022, the contribution to the tax burden from the different forms of tax was still mostly from

indirect tax, which expanded to 40.5%, i.e. 3.6 percentage points more than in the previous year.

On the other hand, the contribution from direct tax fell one tenth to 23.1%. Social contributions

provided 36.5%, 3.4 points less than in 2021.

Below is an analysis of the public sector performance in 2022, according to each level of

administration.

1. Central government

Andorran economy: general developments | VIII. Public sector

The central government (Govern) closed the accounts for 2022 with a non-financial cash

surplus of €72.7 million, a figure that represents 2.3% of GDP and a variation of -198.2%

in homogenous terms when compared with the previous year This deficit correction can

4

be explained by the combination of a steep increase in revenue (+31.4%) and a decrease in

expenditure (-4.1%). These trends were already observed in 2021 with the withdrawal of the

Covid measures and the start of the economic recovery, but were accentuated this year. In the

last 31 years (from 1992 to 2022 inclusive) there have been 24 years in which the Government

ended the year with a deficit and only 7 in which it recorded a surplus, one of these being 2022.

4 In 2022, revenue associated with putting euros into circulation among the country’s banks is recognised in the chapter of investment

income, whereas until 2021 they were included in the chapter of financial liabilities. For comparability, the 2021 figures have been

reformulated to be homogenous with those of 2022.