Page 70 - Economic report 2020

P. 70

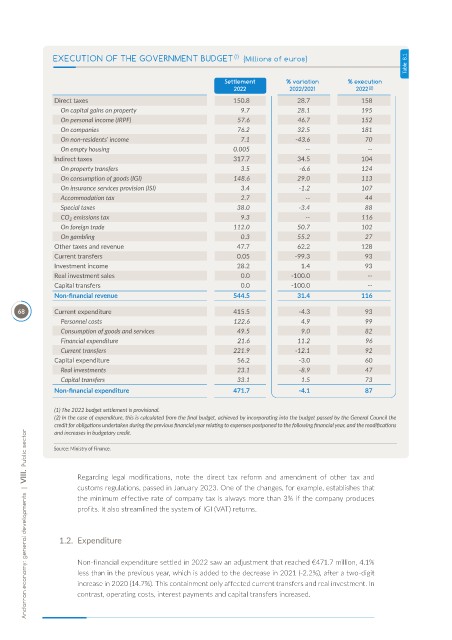

Table 8.1

EXECUTION OF THE GOVERNMENT BUDGET (1) (Millions of euros)

Settlement % variation % execution

2022 2022/2021 2022 (2)

Direct taxes 150.8 28.7 158

On capital gains on property 9.7 28.1 195

On personal income (IRPF) 57.6 46.7 152

On companies 76.2 32.5 181

On non-residents’ income 7.1 -43.6 70

On empty housing 0.005 -- --

Indirect taxes 317.7 34.5 104

On property transfers 3.5 -6.6 124

On consumption of goods (IGI) 148.6 29.0 113

On insurance services provision (ISI) 3.4 -1.2 107

Accommodation tax 2.7 -- 44

Special taxes 38.0 -3.4 88

CO 2 emissions tax 9.3 -- 116

On foreign trade 112.0 50.7 102

On gambling 0.3 55.2 27

Other taxes and revenue 47.7 62.2 128

Current transfers 0.05 -99.3 93

Investment income 28.2 1.4 93

Real investment sales 0.0 -100.0 --

Capital transfers 0.0 -100.0 --

Non-financial revenue 544.5 31.4 116

68 Current expenditure 415.5 -4.3 93

Personnel costs 122.6 4.9 99

Consumption of goods and services 49.5 9.0 82

Financial expenditure 21.6 11.2 96

Current transfers 221.9 -12.1 92

Capital expenditure 56.2 -3.0 60

Real investments 23.1 -8.9 47

Capital transfers 33.1 1.5 73

Non-financial expenditure 471.7 -4.1 87

(1) The 2022 budget settlement is provisional.

(2) In the case of expenditure, this is calculated from the final budget, achieved by incorporating into the budget passed by the General Council the

credit for obligations undertaken during the previous financial year relating to expenses postponed to the following financial year, and the modifications

Andorran economy: general developments | VIII. Public sector

and increases in budgetary credit.

Source: Ministry of Finance.

Regarding legal modifications, note the direct tax reform and amendment of other tax and

customs regulations, passed in January 2023. One of the changes, for example, establishes that

the minimum effective rate of company tax is always more than 3% if the company produces

profits. It also streamlined the system of IGI (VAT) returns.

1.2. Expenditure

Non-financial expenditure settled in 2022 saw an adjustment that reached €471.7 million, 4.1%

less than in the previous year, which is added to the decrease in 2021 (-2.2%), after a two-digit

increase in 2020 (14.7%). This containment only affected current transfers and real investment. In

contrast, operating costs, interest payments and capital transfers increased.