Page 21 - Economic report 2020

P. 21

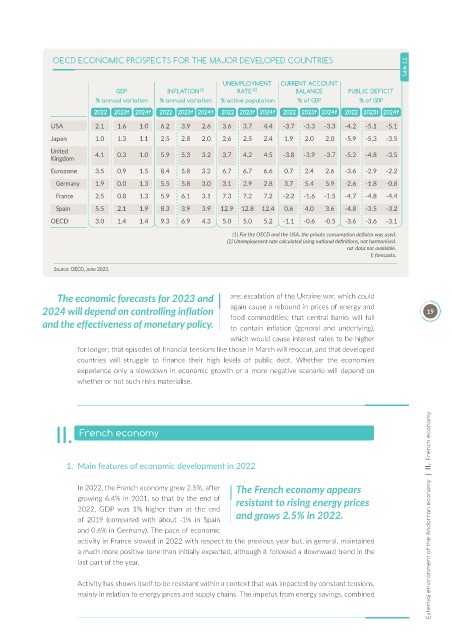

OECD ECONOMIC PROSPECTS FOR THE MAJOR DEVELOPED COUNTRIES

Table 1.2

UNEMPLOYMENT CURRENT ACCOUNT

GDP INFLATION (1) RATE (2) BALANCE PUBLIC DEFICIT

% annual variation % annual variation % active population % of GDP % of GDP

2022 2023f 2024f 2022 2023f 2024f 2022 2023f 2024f 2022 2023f 2024f 2022 2023f 2024f

USA 2.1 1.6 1.0 6.2 3.9 2.6 3.6 3.7 4.4 -3.7 -3.3 -3.3 -4.2 -5.1 -5.1

Japan 1.0 1.3 1.1 2.5 2.8 2.0 2.6 2.5 2.4 1.9 2.0 2.0 -5.9 -5.3 -3.5

United

Kingdom 4.1 0.3 1.0 5.9 5.3 3.2 3.7 4.2 4.5 -3.8 -3.9 -3.7 -5.2 -4.8 -3.5

Eurozone 3.5 0.9 1.5 8.4 5.8 3.2 6.7 6.7 6.6 0.7 2.4 2.6 -3.6 -2.9 -2.2

Germany 1.9 0.0 1.3 5.5 5.8 3.0 3.1 2.9 2.8 3.7 5.4 5.9 -2.6 -1.8 -0.8

France 2.5 0.8 1.3 5.9 6.1 3.1 7.3 7.2 7.2 -2.2 -1.6 -1.5 -4.7 -4.8 -4.4

Spain 5.5 2.1 1.9 8.3 3.9 3.9 12.9 12.8 12.4 0.6 4.0 3.6 -4.8 -3.5 -3.2

OECD 3.0 1.4 1.4 9.3 6.9 4.3 5.0 5.0 5.2 -1.1 -0.6 -0.5 -3.6 -3.6 -3.1

(1) For the OECD and the USA, the private consumption deflator was used.

(2) Unemployment rate calculated using national definitions, not harmonised.

nd: data not available.

f: forecasts.

Source: OECD, June 2023.

The economic forecasts for 2023 and are: escalation of the Ukraine war, which could

2024 will depend on controlling inflation again cause a rebound in prices of energy and 19

and the effectiveness of monetary policy. food commodities; that central banks will fail

to contain inflation (general and underlying),

which would cause interest rates to be higher

for longer; that episodes of financial tensions like those in March will reoccur, and that developed

countries will struggle to finance their high levels of public debt. Whether the economies

experience only a slowdown in economic growth or a more negative scenario will depend on

whether or not such risks materialise.

II. French economy

1. Main features of economic development in 2022

In 2022, the French economy grew 2.5%, after The French economy appears

growing 6.4% in 2021, so that by the end of resistant to rising energy prices

2022, GDP was 1% higher than at the end

of 2019 (compared with about -1% in Spain and grows 2.5% in 2022. External environment of the Andorran economy | II. French economy

and 0.6% in Germany). The pace of economic

activity in France slowed in 2022 with respect to the previous year but, in general, maintained

a much more positive tone than initially expected, although it followed a downward trend in the

last part of the year.

Activity has shown itself to be resistant within a context that was impacted by constant tensions,

mainly in relation to energy prices and supply chains. The impetus from energy savings, combined